Do you really care about your wealth?

Why it's hard for investment advisors to outperform

Last Thursday (January 30), I presented a review on my 2024 Economy & Market Predictions.

I have been studying the economies and markets for over 20 years.

It’s one of those things that is hard to explain to people without them looking at me funny.

You actually enjoy this?

That’s usually what people say to me

Ever since I was little, I was fascinated by the world of money.

How the market works, how to invest, etc.

For years, unofficially, I’m that GUY my friends call when they want to get an update on the economy or my quick opinion on where I think the markets are going.

I’ve attended a number of investment conferences, paid over tens of thousands of dollars on investment research, spoken with several investment fund managers over the year.

Passion matters, especially with investing.

.

Many people I’ve spoken with told me:

I give my money to my investment advisor and they just take care of it.

While I understand the idea of “leaving to the professionals”, I have always believed that no one will care about my money as much as I would.

Caring is an interesting concept.

One can be professional and have all the expertise on a subject, but they may not “care” about their client the same way they would care about themselves.

I believe a large part has to do with how the rewards and incentives are designed in the money managing world.

.

Allow me to peel back the curtain and share some behind the scene stories I’ve learned from many fund managers and advisors.

For most fund managers, especially the ones who manage stocks, they get paid based on performance.

If the fund they managed has done well, they get paid well.

So far so good, interests are aligned with the investors.

Now, investors like to compare apples to apples.

What's the easiest and most common comparison for any stock mutual fund?

The indexes!

These are S&P 500, Nasdaq, Dow Jones Industrial Average, or in Canada, TSX.

In case you're not familiar with the term "index", it's pretty simple.

An index is a combination of the value of the selected stocks.

The S&P 500 Index or Standard & Poor's 500 Index is a market-capitalization-weighted index of 500 leading publicly traded companies in the U.S. - Investopedia

The Nasdaq Composite Index is a market capitalization-weighted index of more than 2,500 stocks listed on the Nasdaq stock exchange. It is a broad index that is heavily weighted toward the important technology sector. - Investopedia

The S&P/TSX Composite Index is a capitalization-weighted equity index that tracks the performance of the largest companies listed on Canada's primary stock exchange, the Toronto Stock Exchange (TSX). - Investopedia

.

If a mutual fund is investing heavily in tech stocks, it's natural for an investor to compare the mutual fund performance to the Nasdaq index.

If the mutual fund outperforms the Nasdaq index, to most investors, that's good!

On the contrary, if the mutual fund underperforms the Nasdaq index, it's "bad"!

Most professional investment advisors are there to help investors properly manage their risks and the return on their investments (rewards).

This is why I put quotation marks around "bad" if the mutual fund underperforms.

To most investors, it may seem bad.

But it's a complete different story if one understands the amount of the risk was taken to create the return.

If the risk was about half of the index, while the return was only 25% less compared to the index, that means the risk/reward is much better to an investor's favor than simply investing their entire wealth in an index.

If only most investors understand this concept.

.

Now that you are aware, this is where it gets interesting.

Let's put yourself in the shoes of your financial advisor or fund manager for a second.

As a financial advisor, if you know your clients are constantly comparing you to the index, and you want to make sure you keep food on the table for you and your family, what's the best thing you would do that will benefit you and your client?

Take a guess?

You would want to make sure your client's investments perform as close to the index as possible.

In other words, you would basically want to help them invest in the index.

Why?

Because you will never get fired if you are performing slightly lower or higher than the index.

Think about it:

If you do better than the index, great!

Your client will like you for that year.

But when next year turns around, and you underperform the index by a bit, the client may stick with you for 1 or 2 more years, and after that, it's hard to keep them staying with you.

.

This is why a pro investment advisor may invest their own money on risker things that could make them a better return but not doing that for their clients.

Or they may be willing to get a lower return with a much lower risk when the market is risky, while keeping their client invested with stocks that track the index.

I'm not saying this is the case for ALL investment advisors or fund managers, however, this is certainly a well known common practice within the industry.

Why am I sharing this with you?

It's simple.

I hope you care about your own wealth.

Because no one else would care about your wealth as much as you do.

.

With that in mind, I'd like to share with you the review of my 2024 predictions.

I'm sharing this with you to give you some perspectives on what's going on in the market and economy.

I believe it’s important to be educated and informed.

Even if someone else is managing your money for you.

Keep in mind, because I don't have a crystal ball, I will never get 100% of these predictions right.

If you want to learn more about the details behind each prediction, you can watch the webinar recording here: https://2024predictionsreview.7to8investors.com

These were predictions I’ve made from 2024.

❌ 1. Liquidity tighten up - Especially for US CRE

✅ 2. Challenging 2 years for US multis (Class B & C) - Price dropping

🤔 3. Interest rate lower in 2024, but not as low/fast as many think

🤔 4. Consumers cut back on spending / defaulting on loans

✅ 5. Deflation for parts of 2024

✅ 6. US/CAN* teeters around recession. CAN - asset inflation

🤔 7. Stocks market corrects 10 - 20%

✅ 8. Wave of small businesses going under => Increase unemployment

✅ 9. Landlords continue to struggle in previously high flying real estate markets. New risk: tenants not paying rent & can’t evict them fast enough

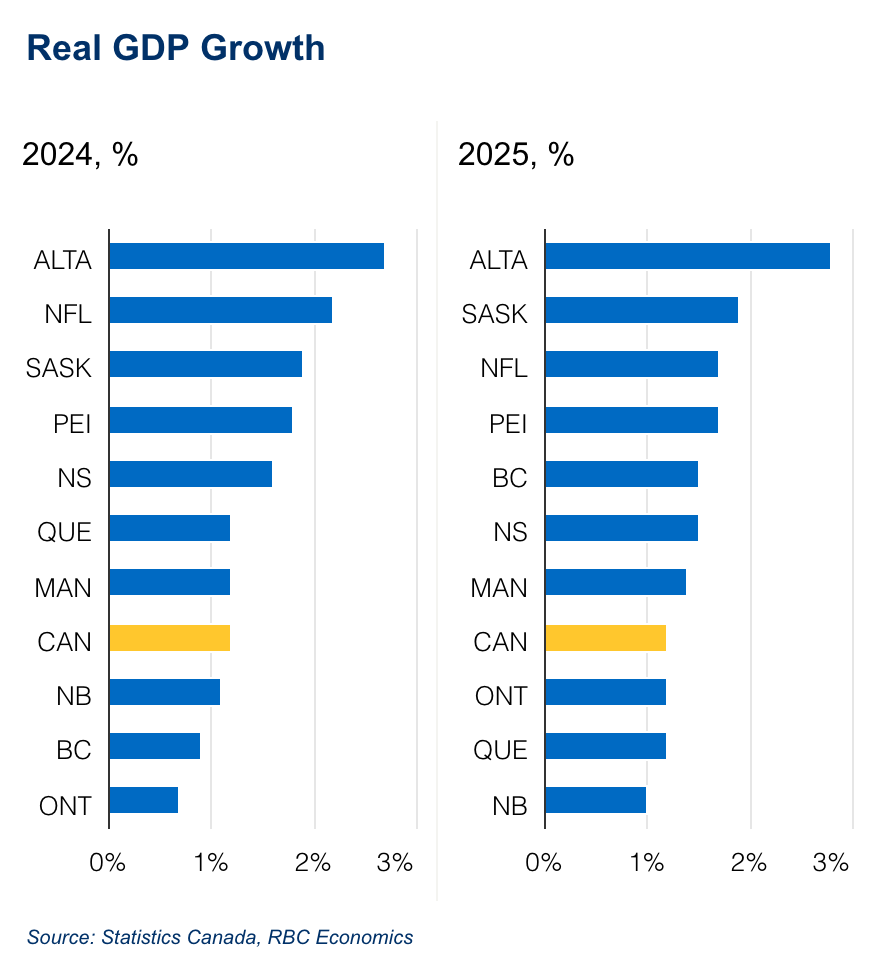

✅ 10. Alberta is calling - with a megaphone

.

Overall, I was happy with how I’ve done, here’s the tally of my report card:

❌ - 1 Missed

🤔 - 3 Partial Right

✅ - 6 Right

.

For the past few years, I’ve been sharing my economy and market predictions publicly.

I study charts, data, patterns and trends to create several investment themes for the year.

These themes result in the “predictions” you see.

I will be sharing the 10 new predictions I’m calling for in 2025 in my upcoming presentation - 2025 Economy & Market Predictions

You can register here to attend this upcoming webinar: https://lu.ma/m1mecayy

If you like my work, I invite you to share it with others.

Eric Chang

Calgary, Alberta

February 4, 2025

Copyright © 2025 Why Alberta Now.

No part of this publication may be reproduced, distributed, or transmitted in any form or by any means, including photocopying, recording, or other electronic or mechanical methods, without the prior written permission of the publisher, except in the case of brief quotations embodied in critical reviews and certain other noncommercial uses permitted by copyright law.

The information provided herein is believed to be accurate and reliable, but Why Alberta Now does not guarantee its accuracy or completeness. The content is for informational purposes only and is not intended to be a substitute for professional financial advice. Why Alberta Now is not a financial advisor and does not provide personalized financial advice. The views and opinions expressed in this publication are those of the author and do not necessarily reflect the official policy or position of Why Alberta Now. The content may be subject to change without notice and may become outdated over time. Why Alberta Now is under no obligation to update or revise any information presented herein.

Investments involve risks, and individuals should consult with a qualified financial advisor before making any investment decisions. Prospective investors should carefully consider the investment objectives, risks, charges, and expenses of any investment before investing.